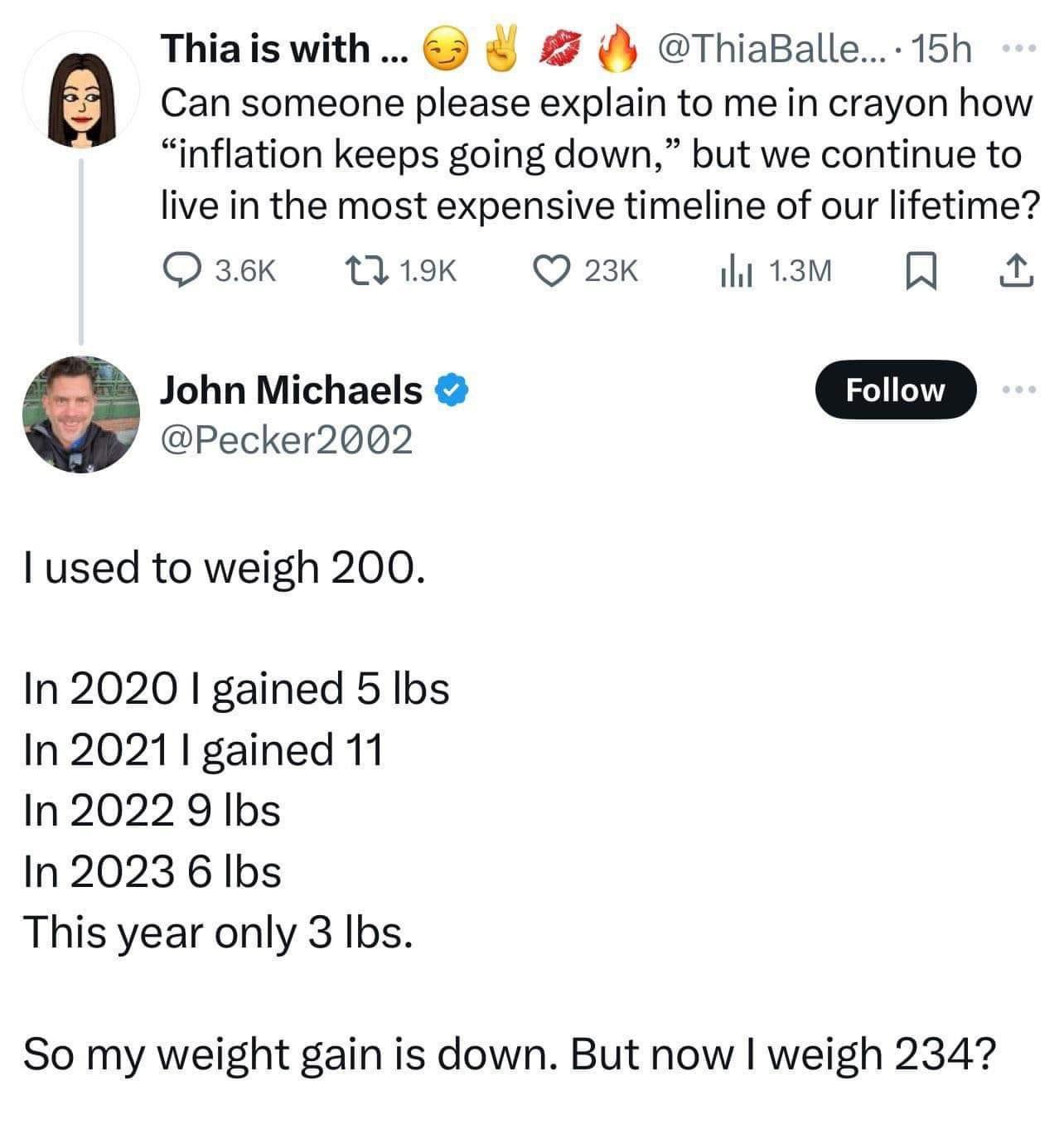

It’s not a common misconception. If you have a fixed rate loan, say a home loan locked in at 3% or 4% (like many current homeowners), then inflation above normal helps you. When your loan was created, a sub 2% inflation rate was priced in. Anything higher than that means you are winning and your lender is losing.

Your advantage is that you can choose to refinance when rates are low, or keep a good interest rate when rates are high. Also, I don’t know what inflation hedges you are talking about that “rich people” have access to. Anyone can buy stocks, real estate, or inflation protected bonds.

What gets priced in is the expected rate, not the current rate. So if we believe 2% is temporarily low, then they’ll price in an inflation rate above 2%. They have more information than you do.

Not everyone can realistically buy the assets you listed. There are tremendous barriers to entry that are dismissed as financial “literacy”.

Inflation isn’t a free money hack for the poor that rich people have left in place out of the kindness of their hearts. It’s why inequality has gotten so much worse since the Nixon Shock.

Yes, it’s the “expected rate” at the time you get the loan. Guess what banks expect when inflation is low? They expect it to stay low. These are fallible people, not emotionless machines.

Banks are run by people who are not going to be around in 30 years when your loan matures. The people who approved all those 3.5% loans in the 2010s do not care that they essentially lose the bank money when inflation is higher. Plus the original bank probably sold the loan to some dumb investors long ago. That’s who takes a bath when interest rates rise (due to inflation).

Most people do not have the option to purchase any of the things you mentioned such as stocks or bonds, as they live paycheck to paycheck, or something close to it. The loans are taken as a matter of necessity, so that much is still relevant.

{kind=link}

It’s not a common misconception. If you have a fixed rate loan, say a home loan locked in at 3% or 4% (like many current homeowners), then inflation above normal helps you. When your loan was created, a sub 2% inflation rate was priced in. Anything higher than that means you are winning and your lender is losing.

Your advantage is that you can choose to refinance when rates are low, or keep a good interest rate when rates are high. Also, I don’t know what inflation hedges you are talking about that “rich people” have access to. Anyone can buy stocks, real estate, or inflation protected bonds.

Sorry but yes it is quite common.

What gets priced in is the expected rate, not the current rate. So if we believe 2% is temporarily low, then they’ll price in an inflation rate above 2%. They have more information than you do.

Not everyone can realistically buy the assets you listed. There are tremendous barriers to entry that are dismissed as financial “literacy”.

Inflation isn’t a free money hack for the poor that rich people have left in place out of the kindness of their hearts. It’s why inequality has gotten so much worse since the Nixon Shock.

Yes, it’s the “expected rate” at the time you get the loan. Guess what banks expect when inflation is low? They expect it to stay low. These are fallible people, not emotionless machines.

Banks are run by people who are not going to be around in 30 years when your loan matures. The people who approved all those 3.5% loans in the 2010s do not care that they essentially lose the bank money when inflation is higher. Plus the original bank probably sold the loan to some dumb investors long ago. That’s who takes a bath when interest rates rise (due to inflation).

Most people do not have the option to purchase any of the things you mentioned such as stocks or bonds, as they live paycheck to paycheck, or something close to it. The loans are taken as a matter of necessity, so that much is still relevant.

That’s not true. Most Americans own some investments. 63% of Middle Class Americans ($40,000 to $99,999) own stocks. 65% of Americans own homes.

https://news.gallup.com/poll/266807/percentage-americans-owns-stock.aspx

https://fred.stlouisfed.org/series/RHORUSQ156N