“Stuck” … yeah I’m stuck, with a bunch of calls, texts and e-mails basically begging me to cash in my equity. I LIKE my house and I make my payments on-time - leave me the hell alone!!

Don’t forget the solar people and house flippers calling from new numbers every week.

And the door to door salespeople. I had a clever one that other day, instead of “could I interest you in a few review…,” this guy pulls out our local netb metering form and asks if we’ve filled one out. Most don’t know what that is and ask, which gives than a way in to pitch solar.

I like the idea of solar, but I’d need to replace my roof given how old it is, and losing those extra years of life just aren’t worth the “savings” or whatever. I also got an independent quote years ago, and it’s still way lower than anything these door to door clowns are offering (granted, they’re after loans, not cash payments).

As a seasoned homeowner, I can now spot them quickly and just say “not interested” and close the door before they can say, “but I’m not a salesperson” or whatever. I’m done being considerate (have had a few people in to give quotes I’m not interested in), so I’m blunt. I have a price in mind, and nobody has gotten within 2x of that.

I have had the same company send their new guys each spring and fall to pitch spraying my house for bugs for half a decade now. New kids same pitch.

I have gone from polite to outright hostile and they keep blowing past my signage since they’re ‘just working on my neighbor’s yard and thought they’d offer out of convenience.’

I treat them just like spam calls. If i didn’t ask you to come, I’m not even opening the door.

Door to door salespeople prey on the “decency” of homeowners to always answer when someone knocks. Stop opening and they’ll stop coming.

All of the solar companies basically charge you $10-15K to act as the general contractor as they sub out the roofing and electrical work. Act as your own GC. You can source your own solar equipment and get a roofer and electrician and you will be able to get as many panels as you want and pay significantly less.

The problem is we have lots of legitimate, unannounced visitors. I have kids, so their friends will come over to play. Our neighbors sometimes drop by for a quick visit. And so on.

I’m unwilling to get something like Ring due to privacy (I don’t trust them), and I’m too lazy to configure something myself (planning to do it this summer, but I’ve said that for years).

So I answer the door. But now I just say we’re not interested, so it’s like a 10s conversation. If they have a clipboard, briefcase, or company uniform, I don’t let them speak, but I do at as politely as I can without wasting anyone’s time.

Act as your own GC

I actually plan to. I estimated my total install would cost something like $10-15k for the system I want. I’d get better panels and inverters than the junk those people pedal, and I’d do some of the work myself (I’d to electrical, but pay a professional to inspect and connect).

Every quote I’ve gotten has been well over $20k cash price, and even more with financing, so that’s a nope from me. If I invest that $20k, I’ll come out ahead vs solar, so it’s not worth it, especially with our low energy prices ($0.13/kWh). So I’ll reevaluate when my roof needs replacing in a few years.

The fed ruined the housing market with their Covid response. They dropped rates to near zero with absolutely no strings attached which let everyone with money maximize their leverage and buy all the housing as investments and drive up prices. The low rates should have been reserved for first time home buyers. Instead, investors went crazy and regular families got screwed with higher prices, and then later, higher rates and higher prices. Unless you bought during the 3 months during 2020 before everything exploded, or owned already and got to refi during Covid, everyone else got screwed.

The US should have looked to Australia as an example of why not to do that. We had very low interest rates pre-covid in a bid to try and drive inflation up to about 2.5%. It didn’t work because it basically meant that people who had plenty of cash just put that into investment properties and drove house prices through the roof, instead of increasing spending throughout the economy like the reserve bank thought it would. That led to a vicious cycle of property investors using the low rates to continue investing in properties, continuing to drive house prices up and pricing new home owners out of the market.

Then, when the post-covid inflation hit, the reserve bank decided to increase interest rates because if the interest rate drops didn’t have an effect on inflation, it should have an effect on inflation in the other direction right? (/s) This meant that the few first home buyers actually got their foot in the door pre-covid were the ones who got punished the most, and the rest of us dealt with the “supply chain issues” (rampant profiteering).

Plus virtually all of the layoffs we’ve had are due to the fed’s decisions.

I bought right before the pandemic and was able to get a slightly lower rate without paying any extra refi-costs during the pandemic.

But my job is extremely stressful, in an industry hit hard by layoffs. My neighborhood was hit hard by tech flight during and post-pandemic, so my home is not worth what I paid.

I’m made lots of good financial decisions and still got stuck as a result of things outside my control!

The Fed eventually ruins everything and is why we are in the position we are now because people who have money purchase investments that are not in the US dollar so that they will go up when inflation hits and people who hold dollars in cash and cash equivalents get fucked. I bought a house in April of 2022 and have a pretty low mortgage rate that I do not intend to give up, just like the article mentions. I’ve just been doing the things required to keep up with maintenance of the house and have already seen my house go up 20% in value just in two years.

This article reframes people being able to afford to stay in their homes as some kind of crisis.

Not present at any point in this article; any evidence that any American is stuck in a home they would rather leave. They couldn’t even be bothered to quote a single homeowner who wanted to move let alone anything indicating that this is a common sentiment.

The only evidence cited are previous rates of housing mobility which are then taken simply as a natural norm with any deviation an unwanted aberration.

The idea that people might generally want to live in the homes they bought long term is not considered. The idea that those who move or downsize are often doing so reluctantly under pressure from their mortgage is not considered.

The average American stay in a home is has been ~8 years.

That number is going to double with rates like this.

Given that the American system is supposed to be a market that’s a bad sign: frozen markets are not efficient markets.

This doesn’t mean people can stay in their homes in a crisis: it means people can’t move. A job the next city over would have to pay thousands more to make selling your home a rational decision. The article says it’s on average $511/mo different.

A crisis still lands you homeless in America.

I’ll grant you that the article is kind of shite, but as someone who is stuck in a house I’d rather be rid of, it resonated with me. I don’t like my house.

We were first time buyers and ended up with a bit of a lemon, which we’ve put a lot of work into but it doesn’t make it a house we love. We’ve been there for 7 years, we tried to move once and COVID fucked it up, and now we’re stuck in a city suburb neither of us really want to live in anymore, in a house that we’re sick of, with neighbors who are growing increasingly conservative that we would rather see the back of. Despite the fact that we’ve technically got over 100k equity on our house now thanks to value inflation we can’t afford a move because even with a 100k down payment any house we actually want is now 450k+ and our monthly payments with a 7-8% mortgage rate would be 3x what our current payment is.

So like, yay, we have a house and at least that’s good, and we’re secure because our payments are low! But also, I want to fucking leave this place, I hate it, I hate my neighbors, I hate this state, and yeah, we’re fucking stuck because even with all our newfound equity we’re still poor af according to the rules of the game and it fucking sucks.

Tax credits? Soy, lame.

Expropiate homes from those who have more than two.

Its funny how capitalists are behaving like low interest rates are a bad thing because people may own homes instead of giving half their income to a parasite.

Parasites don’t care what the interest rates are, they just pass on any excess costs to tenants.

This is the best summary I could come up with:

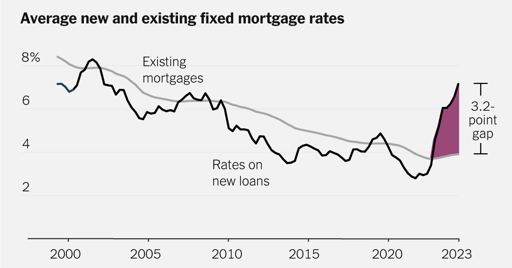

The gap that has jumped open between these two lines has created a nationwide lock-in effect — paralyzing people in homes they may wish to leave — on a scale not seen in decades.

Indeed, according to new research from economists at the Federal Housing Finance Agency, this lock-in effect is responsible for about 1.3 million fewer home sales in America during the run-up in rates from the spring of 2022 through the end of 2023.

Another way to state how unusual this dynamic is: Between 1998 and 2020, there was never a time when more than 40 percent of American mortgage holders had locked-in rates more than one percentage point below market conditions.

Professor Fonseca and Lu Liu at the University of Pennsylvania also find that homeowners who are more locked in are less likely to move to nearby areas with high wage growth.

Some of these effects may sound similar to the years after the 2008 housing crash, when a different problem — underwater mortgages — trapped many people in homes they wanted to leave.

For the homeowners who’ve so far been unwilling to sell, however, that sum is a good deal less than the $50,000 that locked-in rates are effectively worth to the typical mortgage holder.

The original article contains 1,230 words, the summary contains 209 words. Saved 83%. I’m a bot and I’m open source!

Well yeah. I wish I bought 2. I can get a house half the price of my current one and the mortgage will be like $200 more per month.